Global capital flows into private equity continue to exceed expectations. In a thirst for returns, LPs have increasingly relied on the strong performance of private equity to bolster their portfolios. The result was a record-breaking 2017 across a number of metrics. A recently published report by McKinsey indicated that as of 2017, there was an all-time high of $2.8 trillion in private equity assets under management. This includes funds across all private equity asset classes, including: buyout, growth equity, and venture capital. Underpinning the record amount of capital under management is an unprecedented level of ongoing fundraising activity. Bain & Company’s 2018 “Global Private Equity Report” found that approximately $3 trillion of capital has surged into the asset class over the last 5 years.

Fueling the success of the asset class has been strong economic growth in the United States. The economy has grown for 108 months straight. Unemployment is at its lowest level since December of 2000 and consumer confidence is at its highest level since October of 2000. Similarly, public markets in the United States have seen almost unprecedented growth. The S&P 500 and NASDAQ seem to hit near daily all-time highs, with 5-year aggregate returns of 77% and 123%, respectively.

Some economists have been warning that the near 10-year cycle of growth is unsustainable and that the market is due for a correction. Compounding this concern is a lack of consensus on how new policies emerging from Washington will impact the U.S. economy. Furthermore, political gridlock on major issues such as healthcare, infrastructure spending, and immigration reform could present roadblocks for continued economic expansion. Although the future of the economy is somewhat uncertain, there is value in unpacking what a potential cyclical downturn could mean for capital flows into private equity.

Understanding LP Portfolio Composition

There are a variety of different types of limited partners that commit capital to the private equity asset class. These include, but are not limited to, ultra-high net worth individuals, family offices, insurance companies, pensions, endowments, and sovereign wealth funds. While each of these groups may have a slightly different portfolio composition, it’s helpful to understand what a basic LP portfolio looks like.

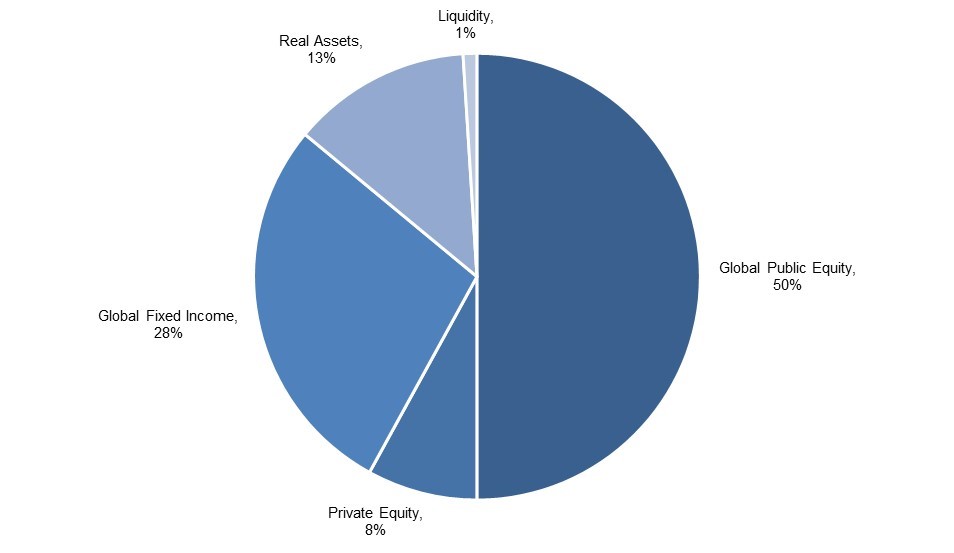

Take for example the California Public Employees’ Retirement System (CalPERS), which was established in 1931, and is the largest non-federal pension fund in the United States with $351 billion under management as of June 2018.

Figure 1 – CalPERS Target Asset Allocation

The Future of LP Contributions to Private Equity

Bain & Company found that 95% of private equity LPs experienced returns that met or exceeded their expectations. A survey by Preqin found that 92% of LPs plan to devote either an equivalent amount or more to private equity over the next 12 months. Further, in the same study, 96% of LPs indicated a plan to maintain or increase their private equity allocation over time.

However, unpacking this further provides more clarity on the causation of these trends. Strong returns in global public equities have resulted in the need to funnel capital back into other asset classes to maintain the correct allocations. Due to fund governance, investment professionals must regularly rebalance their portfolios to ensure consistency with mandated allocations. In effect, part of the reason for record-breaking capital flows into private equity are strong economic growth and above-average public market returns of late.

To explore this line of thinking further, what would be the effect on capital flows into private equity in the event of compression in public equity valuations? Particularly, given that private equity valuations are less responsive to market changes how would LPs respond? For example, if the public markets experienced a 20% correction in valuations, a similar correction in private equity asset values—particularly as it relates to the carrying value of existing portfolio company investments—would not occur until ownership positions were exited. By extension, LP capital flows would need to be redirected to now underweight areas of the portfolio mix until a new equilibrium is achieved.

All of this is not to say that private equity hasn’t been a strong performing asset class for LPs. It will continue to be a cornerstone of their investment and diversification strategy going forward. However, it is important to fully understand the myriad factors that influence capital flows into and out of the asset class.

LP Concerns and the Path Forward

There are a variety of other factors which continue to inform and influence the flow of capital into private equity. In Preqin’s annual survey of institutional investors, 63% indicated having a positive perception of private equity. Although still relatively high, this represents a 21% decrease from the same time a year earlier. Roughly 88% of those surveyed identified valuations as a key issue for private equity in the years to come, with 37% feeling that portfolio companies are currently overpriced and that a market correction is likely. Other major concerns include the attractiveness of the exit environment (40%), fees (39%), and deal flow (30%).

Data behind the rise in private equity valuations continues to stack up. While deal volume has remained relatively flat, deal value continues to rise, indicating a continuous increase in multiples paid. According to PitchBook, median EV/EBITDA multiples rose to 10.7x in 2017, up from 9.2x the year prior. With roughly $1 trillion in dry powder available, there is no expectation for this trend to slow down.

Increased valuations within venture capital were even more striking. Preqin found that deal volume decreased for the fourth year in a row, yet deal value increased by 28% to an all-time high. As a result, LP sentiment for venture capital has decreased. Only 34% of LPs surveyed in Preqin’s study have a positive perception of venture capital, down from 41% in 2016.

Another emerging trend among large LPs is segmenting a portion of their private equity capital for direct investments. In May 2018, CalPERS announced its plans to pursue a direct investment model to drive better returns when compared to a fund-only investment model. Similarly, the British Columbia Investment Management Corporation (BCI), which manages in excess of $145 billion has launched a comparable program. Over the last 5 years, large family offices have evolved along a similar path, opting for direct investment opportunities to avoid fees and capture a large share of overall returns.

A Bright Spot on the Horizon

As valuations in traditional buyouts continue to rise and the dispersion of VC returns accelerates, LPs will need to find new ways to diversify into attractive asset classes. One area that has consistently shown promise is growth equity. As a standalone, established asset class, growth equity is a relatively new phenomenon. In its early days, growth equity investors were often playing either up- or down- market from existing investment strategies. In recent years, growth equity has seen an increase in focus due to its focus on less risky and more established, yet still high-growth businesses.

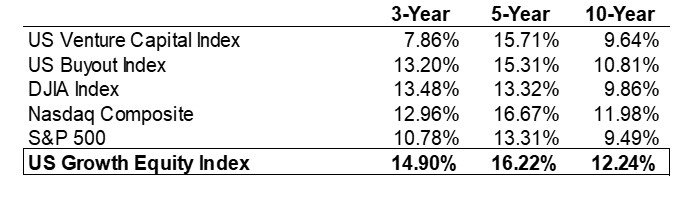

McKinsey & Company’s 2018 report indicated that North American firms had $121 billion in growth equity assets under management. This is still less than the $327 billion in VC and ~$1 trillion in private equity assets under management. However, the burgeoning asset class has consistently posted attractive returns. As seen in Figure 2 below, on an aggregate basis, growth equity has produced returns above other benchmarks.

Figure 2 – Cambridge Associates Benchmark Returns Analysis (March 31, 2018)

With upwards pressure on valuations having no signs of slowing, LPs will be increasingly focused on finding new investment strategies to generate returns. Growth equity’s blended risk profile relative to VC and buyout strategies, as well as its superior return history, make it a likely destination for increased LP investment.

Discover unique insights from growth investors and leading executives.

Sign up for our weekly newsletter.